In a post entitled Trends in Supply Chain Software, I presented thoughts on the future of supply chain software drawn from two analysts, Mary Shacklett, founder and president of Transworld Data, and Lora Cecere, a partner with the Altimeter Group. Both Shacklett and Cecere were excited by the potential of emerging technologies. Tim Payne, Research Director at Gartner, isn’t so sure. He headed a research effort that looked at the hype surrounding Supply Chain Management (SCM) technologies. During an interview with a staff member of the Financial Times, he answered some questions about the study [“Supply chain management hype cycle,” 25 January 2011]. According to the article, one of the purposes of the study was to help business executives “understand the potential for those technologies to change the shape or direction of their industry.” Hence, the first question was: “Based on Gartner’s research, what is the most hyped supply chain technology?” Payne responded:

“Sales and operations planning (S&OP) and/or integrated business planning solutions are probably the most hyped SCM technology at the moment. S&OP has been around in supply chain circles for decades, but it increasingly being seen as a key process for managing value trade-offs across an integrated value chain as part of company’s drive to become demand-driven and improve supply chain effectiveness and business value. Gartner’s supply chain research is positioned under our umbrella model of Demand-Driven Value Networks (DDVN) as a model of supply chain leadership (it also underpins our ‘Top 25’ supply chain research). As with all business strategies and processes there are stages of maturity to go through before you achieve maximum business value. The same is true of DDVN and also for supporting processes such as S&OP.”

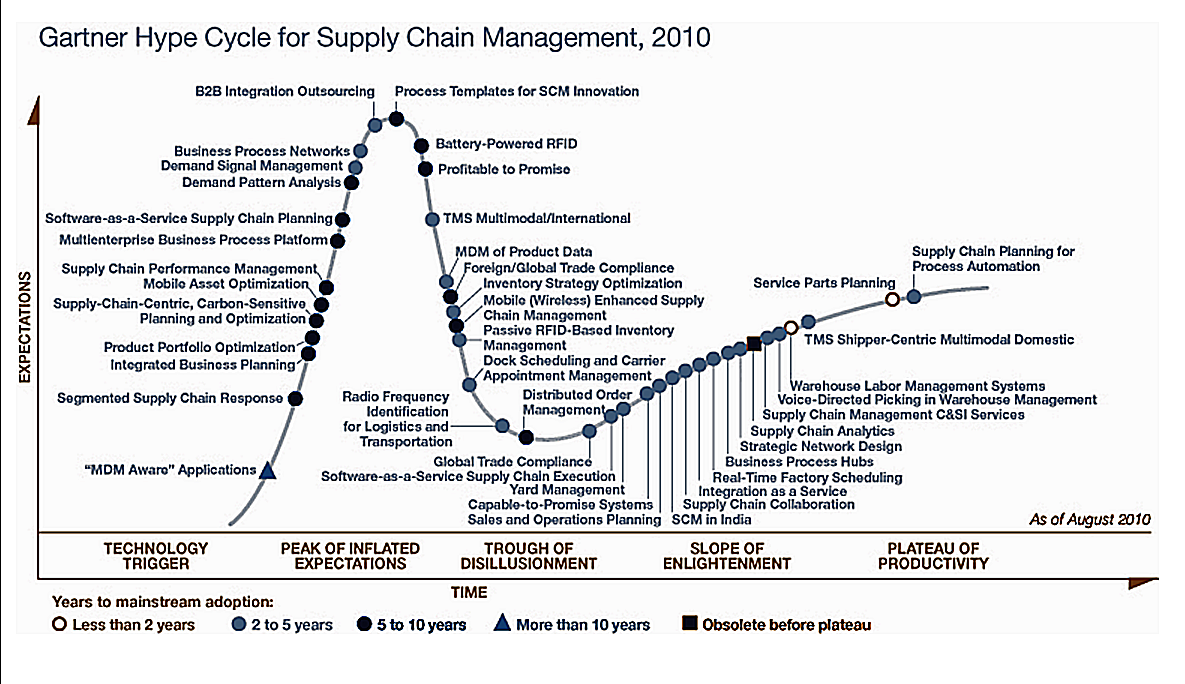

Let me insert a couple of comments before continuing with Payne’s response. First, if you want to learn more about S&OP, read my posts entitled Some Thoughts Concerning Sales & Operations Planning, Part 1 and Part 2. Second, what Payne calls Demand-Driven Value Networks (DDVN) are more often called demand-driven supply chains. To learn more on that subject, read my post entitled, Demand Driven Supply Chains. That post also discusses more about S&OP. On several occasions during the interview, Payne refers to a “hype cycle” and to where particular processes rest on the cycle’s graph. Below is a copy of the “hype cycle” that accompanied the article. Referring to the graphic should provide you with a better understanding of what Payne is saying.

Payne continues his answer to the question: What is the most hyped supply chain technology?

“In the lower levels of DDVN maturity (more akin to traditional internal supply chain management) the S&OP process is likely to be an operationally focused demand/supply matching process (we show this as the S&OP technology profile on the 2010 SCM Hype Cycle in the slope of enlightenment) and many companies have this type of S&OP process in place today. However, those organizations that are driving towards DDVN and are at a higher level of process maturity are typically moving their S&OP processes to higher levels of maturity also, and in some cases towards the beginnings of integrated business planning (IBP). We show this on the 2010 SCM Hype Cycle as the IBP technology profile which is firmly in the technology trigger zone of the cycle. IBP offers companies the opportunity to link planning across different domains, from operational, through tactical, to financial and strategic planning. In most companies today there is still a massive disconnect between strategic planning and what happens at the operational level. Even with an S&OP process in place this gaps typically exists.”

From what I’ve read, most supply chain analysts agree with Payne that large “white spaces” exist between current supply chain technologies and the ultimate objective of a demand-driven supply chain that is supported by integrated business planning. Companies working to fill those white spaces have a ways to go, but many of them, including Enterra Solutions®, are working on systems that can be rightfully placed on what Payne calls “the slope of enlightenment.” Payne continues:

“IBP is seen to connect S&OP through to Corporate Performance Management (CPM) and to facilitate the development and evaluation of feasible, and financially modelled, strategic initiatives that can illuminate alternative operational models that better support the achievement of strategic goals. Today, there are no fully baked IBP solutions in the market, although some of the more advanced S&OP solutions are evolving in that direction as well as a couple of emerging niche vendors. There are also other analytical applications that are emerging that support the modelling and analysis aspects of a IBP/high maturity level S&OP process – technologies to support processes such as how to segment and design your supply chain for maximum value creation; how to optimize your product portfolio to maximize profitability; how to analyze demand patterns to gain better market insight that can be driven into models for determining a profitable response to such patterns. What these emerging SCM technologies have in common is their strong analytical nature and provide evidence of a continuing convergence between process-orientated business applications and analytics-orientated business intelligence capabilities. In many ways, these emerging SCM technologies are showing signs of possessing pattern-based strategy capabilities in the way they can help companies seek patterns, model the impact of these patterns and offer ways in which the organization can adapt to maximize return/minimize risk of the identified patterns.”

The bottom line right now is that “there are no fully baked IBP solutions in the market.” There is, however, a lot of talk, a lot of potential, and a lot of hype. Nevertheless, I believe most analysts would say that companies are moving in the right direction. More on that later. The second question posed to Payne was: “[Are there] any other SCM technologies that you would specifically call out as likely to have a significant business impact that executives should monitor?” Payne responds:

“I’ve mentioned several of these above in the way that they support an evolving IBP process for an organization. Perhaps of those the one that offers significant business impact, either as part of an IBP process or as a standalone capability, is what Gartner calls segmented supply chain response. In essence this is the recognition that one-size-does-not-fit-all when it comes to the supply chain. Now supply chains have been doing demand and supply side classifications for years, but what leading companies are discovering is that this segmentation needs to be expanded to encompass much more of the supply chain, and ideally needs to be end-to-end in definition. These companies need technologies that help with the design and evaluation of different supply chain configurations that support different performance capabilities that can be matched with relevant customers and products. We are seeing a lot of interest in segmentation from the business side of supply chain (especially in industries such as high-tech and consumer goods) but the technology side is lagging behind. Executives need to monitor the evolution of technologies to enable robust segmentation processes and learn how to leverage them for supply chain advantage.”

Payne makes an excellent point. Too often people refer to “the supply chain” as though there were only one of them. Not only are there multiple supply chains supporting unique industry sectors, but, as Payne points out, within a company there can exist multiple supply chains. This is becoming more true as retailers adopt business models that support multiple sales channels. The third (and final) question posed to Payne refers to the hype cycle graphic: “Should business leaders ignore those SCM technologies that are in the ‘trough of disillusionment’?” Payne responds:

“Definitely not. In fact, this can be an opportunity to progress in ‘stealth’ mode while the technology is out of fashion. Often these technologies offer significant value to the supply chain but perhaps not at the levels extolled when the technology was at the peak of its hype. A great example is RFID – which has a valuable place in the supply chain, but is not a panacea for all the ills of supply chains as previously hyped. Many of the SCM technologies in the trough of disillusionment are focused on the execution side of supply chain management; several with a globalization flavor to them as well. These are valuable technologies to support a more integrated and responsive execution capability as part of a journey towards DDVN, but some companies have struggled to transform their organizational structures and business processes to successfully leverage these technologies on a broad scale and have had to often narrow their focus in order to deliver tangible business benefits whilst recognizing the limitations of the existing technologies.”

Many analysts would agree with Payne that companies ignore technologies in the “trough of disillusionment” at their own risk. I like his example of RFID tags. To learn more on that subject and why companies shouldn’t ignore it, read my post entitled Two Views on the Future of RFID Tags. Earlier, Payne mentioned the fact that Gartner annually publishes a list of the Supply Chain Top 25. He said that Gartner’s vision of Demand-Driven Value Networks underpins its ‘Top 25’ supply chain research. Kevin O’Marah, chief strategy officer at Gartner, explains in an interview with the Financial Times that “the supply chain touches many sides of the business and has become a strategic weapon.” Click the link to hear the entire interview.

Gartner indicates that two themes emerged from its review of the 2010 Top 25 winners: “A re-examination of the benefits of vertical integration and increasing advances in the realm of sustainability.” The analysis group then provides a short list of recommendations that companies can follow to improve their supply chains:

- “Apply demand-driven principles to coordinate and integrate the functional areas of supply, demand and product management in order to better sense, shape and respond to changes in market demand.

- “Take a cue from the leaders when designing your own supply chain strategy. Think outside in, starting with your customers and working back through your trading-partner network to design a profitable response. Remember that one size does not fit all. Define how many supply chain types you have and design a customized response for each.

- “Balance operational excellence with innovation excellence for superior overall performance.

- “Focus on acquiring, mentoring, growing and retaining supply chain talent.

- “Measure your supply chain as your customer experiences it. Use the right supply chain and product metrics to consciously manage performance, and foster a culture that embraces measurement for continuous improvement.”

Just in case you are wondering, here are Gartner’s 2010 Supply Chain Top 25: 1) Apple; 2) Procter & Gamble; 3) Cisco Systems; 4) Wal-Mart Stores; 5) Dell; 6) Pepsico; 7) Samsung; 8) IBM; 9) Research in Motion; 10) Amazon.com; 11) McDonald’s; 12) Microsoft; 13) The Coca-Cola Company; 14) Johnson & Johnson; 15) Hewlett-Packard; 16) Nike; 17) Colgate-Palmolive; 18) Intel; 19) Nokia; 20) Tesco; 21) Unilever; 22) Lockheed Martin; 23) Inditex; 24) Best Buy; 25) Schlumberger. Gartner believes that supply chains have added significant value for these companies and have been an important part of their success.