Last year, Dan Gilmore, Editor-in-Chief of Supply Chain Digest, wrote, “Even though most of us are … generally aware of … supply chain finance matters, … I would say most supply chain professionals are only modestly knowledgeable at best in terms of the details.” [“A Little Supply Chain Finance 101,” 3 June 2011] In order to address this shortcoming, Gilmore provides a brief primer starting with a discussion of working capital. He writes:

“Part of the confusion is that the term sounds like it is a good thing – I’d like to have a little more ‘working capital.’ But it isn’t. Working capital is basically the amount of cash a company has tied up just running the business. The more that is tied up, the less cash is available to do something else with, or the more a company has to borrow to fund its operations.”

The particular focus of Gilmore’s discussion of working capital involves resources tied up in inventory. “Inventory levels,” he writes, “are the most prominent way the supply chain can affect working capital.” He continues:

“Inventory is … a key indicator of supply chain excellence; the area where supply meets demand. Where it gets confusing to most of us is that changes in inventory levels impact key financial statements differently. Let’s say a company holds on average $1 billion in inventory. Let’s further state that through various initiatives, it is planning to reduce those inventories 10%, or $100 million. What will happen on the three key corporate financial statements (the balance sheet, income statement, and cash flow statement)? Inventory levels on the balance sheet would decline by $100 million. Cash flow on the cash flow statement would also increase by $100 million – a dollar for dollar improvement. This would happen because working capital would be reduced by $100 million. The reduced inventory would move from being tied up in working capital [and would] turn into cash.”

So far Gilmore believes that things are pretty straight forward. “The trickier thing,” he writes, “is what would happen on the income statement. Does having lower inventory improve profitability as well as improving cash flow?” He continues:

“Well, it certainly is assumed to do so for most companies when estimating the payback from various initiatives. For an easy and timely example, when calculating the benefits of low cost country sourcing, the lower unit price obtainable of course has to be balanced with extra costs for transportation, duties, etc., plus the costs of holding additional inventory due to the longer supply chain, more supply uncertainty, etc. Now, what should that cost of inventory number be? And frankly, I will say that there is the theoretical number and then ultimately the actual number that will eventually show up (or not) on the real future income statement.”

Gilmore notes “that a key driver of total US logistics costs is the cost of holding inventory.” He further notes that the cost of holding inventory “can vary significantly from year to year, based primarily on interest rates.” He continues:

“There are actually several potential ways to calculate the cost of inventory relative to the income statement:

“1. What it costs a company to borrow money. …

“2. The company’s ‘cost of capital’: this gets a bit trickier (going into something called weighted average cost of capital, for example), and basically means the return shareholders expect from the company’s use of capital. Varies from company to company, but let’s say in general it ranges from 8-12%.

“3. Inventory carrying costs: interest costs or cost of capital plus all the other costs associated with inventory (storage, handling, obsolescence, insurance, taxes, shrink, etc.).”

Gilmore reports that Georgia Tech professor, Dr. Stephen Timme, believes “that most companies underestimate true inventory carrying costs.” Gilmore notes that the Council of Supply Chain Management Professionals (CSCMP) estimates “inventory carrying costs for 2009 were calculated at about 19%.” Theoretically, that means a company should see a top end increase of $19 million on a reduction of $100 million of inventory. The question Gilmore asks, “Would those increased profit dollars really show up on the income statement?” He says that is valid question because the cost of carrying inventory “is not an income statement item.” He continues:

“Supply chain financial consultant Gerry Marsh of High-Tech Analyst Group told me, … ‘As you correctly point out, this $19 million savings will never be seen in the income statement because only some portion of the carrying costs represent a reduction in operating expense (which goes through the income statement). The capital reduction benefit goes through the cash flow statement. Nevertheless, converting the capital reduction benefit of $100 million into an annual benefit by multiplying it by an annual cost of capital figure is not unreasonable.'”

Gilmore states that Marsh has convinced him “that reducing inventory and improving cash flows has an positive impact on a company’s valuation or stock price beyond just the impact lower inventory carrying costs will have on profits/earnings per share.” We all know, however, that reducing inventory dramatically carries some risks. The question is: How much inventory should be maintained? Sandeep Deolekar notes that inventory is maintained “as a buffer” against two competing forces:

He states that the more “stages or echelons in an end-to-end Supply Chain” the more inventory there is that must be carried. [“Is Inventory the ‘necessary evil’?” Supply Chain Management, 5 July 2011] Lora Cecere writes, “My observation is that while most companies focus on the level of inventory–how much inventory is the right amount–for their supply chain, supply chain leaders go one step further to focus on form and function of inventory.” [“HEH?” Supply Chain Shaman, 3 November 2011] She explains what she means by “form” and “function”:

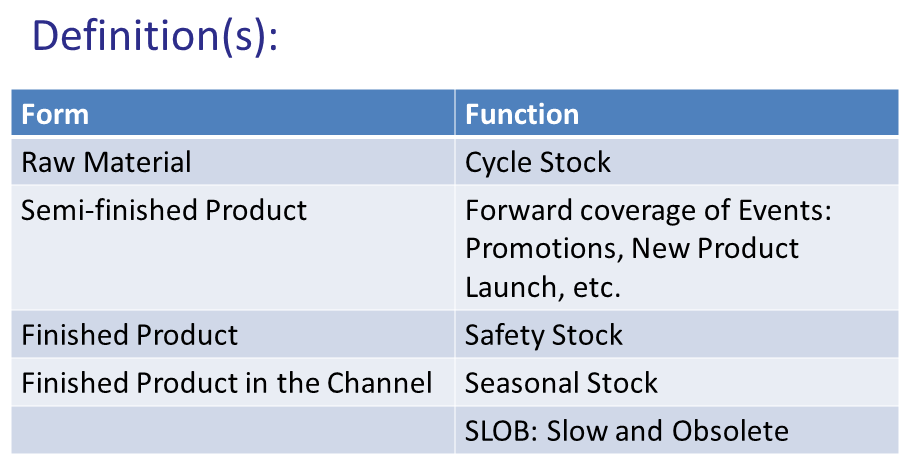

“The form of inventory is the state in which it is stored. Inventory can be stored as raw materials, semi-finished goods and as a finished good or final assembly. The further back in the supply chain that inventory is stored (e.g., raw materials), the greater the supply chain flexibility.

“The function of inventory is the role that the inventory plays in the supply chain. There are many forms – cycle stock, seasonal inventory, event pre-builds – that need to be managed.”

Cecere demonstrates these distinctions in the following figure.

Cecere indicates that she often asks company executives how their decisions affect cycle stock and that many decision makers are surprised by the question. She continues:

“While most companies talk of safety stock (the decision to hold inventory to buffer supply and demand variability), I find that few companies understand the principles of cycle stock. Cycle stock, the inventory that is necessary to cycle through products or from manufacturing to distribution cycles, is often a missed opportunity. Or decisions are made that increase the need for cycle stock without thinking through the impact.”

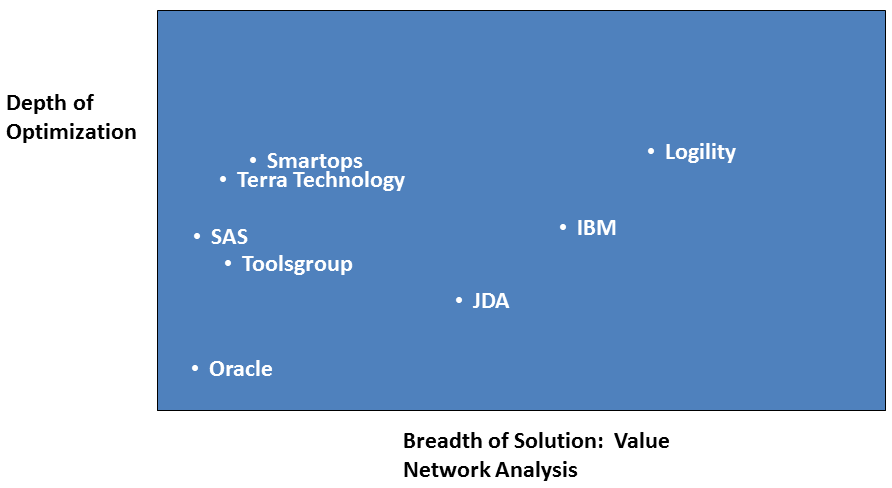

She notes that “there are a lot of technology solutions in the market to improve inventory optimization.” She indicates that some of these solutions address the “form” side of inventory while others address the “function” side. She provides her view of the inventory optimization industry in the following graphic.

Cecere indicates that “the lasting impact happens when people understand the impact of supply chain decisions on inventory and working capital.” Like Gilmore, however, she reports, “I am constantly surprised in my travels how little most financial teams understand about the trade-offs of supply chain planning and what defines supply chain excellence.” Like other analysts, Ralph Cox, Principal at Tompkins Associates, notes, “Inventory policies drive two types of costs: period operating expenses and working capital requirements. … [While] most individual companies have succeeded in reducing inventory levels; total logistics costs per hundredweight are increasing, and inventory costs as a percent of total logistics cost are increasing.” [“25 Ways to Lower Inventory Costs,” Modern Materials Handling, 28 July 2011] As the title of his article indicates, he offers some strategies that can be used to address inventory costs. He writes, “Some of these strategies address having less active inventory, others how you acquire active inventory, and still others require transferring inventory or relying on vendors for better inventory management.” It is a fairly comprehensive list and certainly worth checking out.