In several past posts, I’ve predicted that the multinational companies that will do the best in the future are those that transform themselves into what IBM’s Sam Palmisano calls “globally integrated enterprises.” Cargill is a multinational company that is learning this lesson the hard way. Gregory Page, Cargill’s CEO, “admits the group’s failure to integrate its diverse businesses has been frustrating for customers and made it hard to avoid duplication” [“All you can eat,” by Javier Blas and Gregory Meyer, Financial Times, 19 May 2010]. Page asserts that, “as Cargill moves to strengthen its leading position in a crucial global market, … an array of operating units must co-operate better.” Blas and Meyer write:

“A decade ago, after profits halved, the company set out to offer more than just bids and offers for the farmers and food companies it serves as middleman. Instead of counterparties, Cargill now calls them customers – people with whom, as one executive puts it, ‘we need to be more open, transparent and vulnerable’. In many senses, Cargill is one of the hidden companies of the global economy. As the world’s agribusiness leader, it sits at the nexus of one of the world’s biggest and most critical industries – a force of great importance to millions of farmers as well as to large food multinationals from Nestlé to Coca-Cola and Kraft, though it [is] much less well-known as a name. Its significance – as the equivalent of ExxonMobil for the agriculture markets – is set to increase further as food demand rises in China, India and in parts of the developing world, and the use of biofuels grows in the west.”

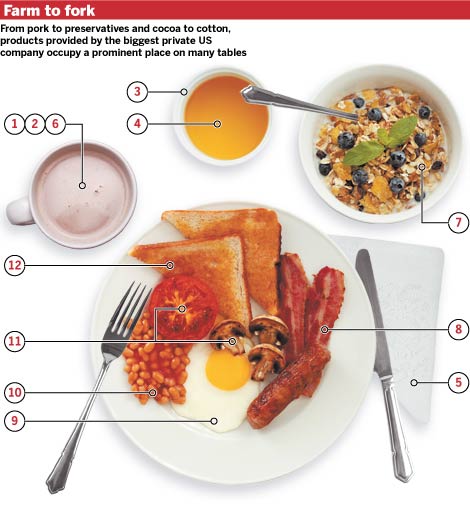

To give you some idea of how broadly Cargill’s reach is felt, the paper provided the image below (which is more of a typical English breakfast than an American one) and then discusses Cargill’s role in getting that food on the plate or in the cup.

1. The world’s largest cocoa trader, Cargill also processes the beans into cocoa liquor, butter and powder, the raw materials for chocolate.

2. The world’s largest sugar trader, Cargill buys from countries such as Brazil and selling to Egypt, India, China, Russia, Ukraine and others.

3. Cargill is developing a business focused on replacing petrochemical-based plastic products with soya-based products.

4. Cargill produces sterols, plant compounds that help cut cholesterol levels, used in orange juice and other products.

5. Cargill merchandises cotton worldwide, buying and sell cotton in North America, Europe and Asia and operates cotton gins in Africa.

6. Animal feeds are supplied by Cargill to commercial dairy farmers in 28 countries across North and South America, Europe and Asia.

7. The world’s largest corn processor, Cargill handles about 20 per cent of the US crop.

8. Cargill Pork is involved in pork production in the US and export.

9. Cargill Kitchen Solutions is a leading marketer of high value, processed egg products in the US.

10. From seasoning used in processed foods such as baked beans to the kind used on frozen roads, Cargill produces more than 1,000 types of salt.

11. Through its subsidiary, The Mosaic Company, Cargill is a leading producer of fertilisers, supplying fruit and vegetable farmers around the world.

12. Cargill’s grain and oilseed subsidiary trades grains and employs 15,000 people in 50 countries, operating 324 silos and 31 import-export terminals.

By any measure, those are some pretty impressive facts. As the global population pushes towards its peak around the year 2050, the importance of and business opportunities in the agricultural sector will only increase. Blas and Meyer continue:

“Agriculture and the big food trading houses have been drawing increased attention from policymakers following the price spikes and supply uncertainties of the 2007-08 global food crisis, the first in more than 30 years. Food security, long a topic merely for agriculture ministers, is now hotly debated among leaders of the Group of Eight industrialised countries. Amid all this profound change surrounding its business, Cargill has had to do more than just alter its language. It has spent several years expanding down the supply chain from its large-volume, thin-profit business of trading bulk agriculture commodities – instead transforming some of the raw materials into ingredients it could sell at a premium. In addition, the group is nowadays much more than a grain trader. An industrial side that mines salt, makes plastic from plants and includes a majority stake in Mosaic, the fertiliser company, provides a chunk of the profits. The company holds dozens of patents, including one recently granted for a process to prevent scrambled eggs from turning mushy. Cargill’s animal nutrition labs formulate feeds that colour hens’ eggs from white to tan, a spectrum its sales people pitch with the kind of card-stock fan to be found at paint stores. Its investment vehicles trade across asset classes on behalf of institutional investors and provide administration services to complex hedge funds, while the company advises farmers and large food companies on hedging against the risks inherent in crops and markets.”

In my discussions about development, I have often noted that countries whose economies rely on the sale of commodities have a difficult time achieving a sustainable economy because the volatility of commodity prices makes it difficult to plan for the future. My advice, like the advice of so many others, is to diversify. Cargill’s size makes it easy to compare it to a small country. Like a country with a commodity-based economy, Cargill found itself in a situation where relying on the purchase and sale of agricultural commodities tied its future to the vagaries of the market as well. But, as the above paragraph describes, Cargill’s leadership diversified the company’s business beyond commodities and is in a much better economic position to thrive. Blas and Meyer continue:

“Ray Goldberg, a professor at Harvard Business School, wrote in a case study that the transformation made Cargill ‘less subject to competition and, consequently, its margins and profits would be more stable and secure’. Still, the biggest slice of Cargill’s earnings comes from its global trading business – the network of ships, silos, warehouses and people who help move vast tonnages of wheat, corn, oilseeds, cotton, cocoa and sugar around the world. Indeed, in the teeth of the global recession, the past three years are shaping up to be the best in Cargill’s 145-year history. Helped by the new ‘farm to fork’ approach, the group is set to earn almost $10bn in the 2008-10 period, up from $1.5bn in 1998-2000 when the shake-up, called “strategic intent 2010”, was launched. With nearly $117bn in revenues last year and 138,000 employees based in 67 countries, Cargill also ranks as America’s biggest privately owned company. Founded in 1865 with a single Iowa grain elevator, the group remains controlled by about 80 members of the Cargill and MacMillan families, the low-profile descendants of founder William Cargill.”

It’s worth pausing here to make point. In my numerous posts about the economy, I have insisted that job creation should be at the top of government’s list of priorities. The government itself shouldn’t be creating the jobs; however, it should be establishing conditions that foster entrepreneurism. Cargill is a great example of the kind of impact that entrepreneurs can have. Over the past century and a half, Cargill has grown from a small firm with one grain elevator to global company employing 138,000 people. That’s a pretty impressive record. Blas and Meyer note that the company’s current CEO wants to ensure that the company makes an even greater impact in the future. Blas and Meyer continue:

“To invest and grow, Cargill depends on keeping its earnings ahead of funding costs. ‘We went from being several points under the cost of capital returns to several points over,’ Mr Page tells the Financial Times in a rare interview at the company headquarters in Wayzata, Minnesota.”

Blas and Meyer note that when any company gets really big, people start worrying that it is too big. How often have you heard the phrase “too big to let fail” during the current financial crisis? Those concerns are now being focused on companies like Cargill. Blas and Meyer explain:

“The effort to add more value to the workaday business of trading commodities has not extinguished doubts that an industry concentrated in a few large hands harms farmers. These days, US antitrust authorities are holding workshops … looking into potentially anticompetitive market power among agricultural buyers and processors. And when food prices spiked in 2007-08, activists criticized the trading houses for profiteering from the crisis. Cargill’s response was to lift some of the veil of secrecy, showing how the company moves crops around and advises some of the world’s governments about when and how to buy or sell, and from or to whom. Without its input, came the message, crop surpluses might rot in Brazil and hunger could hit Egypt.”

Cargill’s executives have discovered the magic of connectivity and information sharing. As the global population rises, the climate continues to change, water scarcities increase, and food security concerns grow, sharing information about where and when food is available will be critical to optimizing the agricultural sector and the supply chains that support it in the decades ahead. Blas and Meyer note that Cargill isn’t without competitors:

“The group’s main competitors include Illinois-based Archer Daniels Midland, New York-based Bunge and France’s Louis Dreyfus. The four, known because of their initials as the industry’s ‘ABCD’, dominate global flows of agricultural raw materials. But other companies have entered the top league as food demand surges in emerging countries: among them are Wilmar and Olam International, both of Singapore, and Hong Kong-based Noble Group.”

To gain a competitive edge over its competition, Cargill executives realized that they needed the best information they could obtain and that the data needed to get into the right hands at the right time. They also recognized that they already access to an incredible amount of information.

“Cargill boasts about the intelligence the trading operation gives it in anticipating markets. Through its involvement in ocean shipping and trading basic materials – which also include nonagricultural commodities from crude oil and natural gas to iron ore and coal – the company says it had an early peek at the looming economic slowdown. ‘The insights gathered from many activities and places enabled our trading teams to avoid being stung by plummeting commodity prices’, its 2009 annual report says. Trading is, however, a brutal business even for Cargill. As grain prices surged in 2008, with corn reaching a record above $7 a bushel, a combination of the credit squeeze and demands for extra money to cover its futures hedges forced Cargill temporarily to stop buying farmers’ grain for deferred delivery – an unprecedented move. Though it continued to conduct spot trades, the extra collateral that exchanges required in the forward market as prices went up would otherwise have run into hundreds of millions of dollars for a company of Cargill’s size.”

Blas and Meyer go on to detail some of the economic scares the company has survived and note that Cargill’s economic health is highly dependent on an expanding global economy. They also note that Cargill “is not immobile” while waiting to find out whether the global economy will recover.

“Cargill has launched a new master plan, labelled ‘strategic intent 2015’, to further the process of change. For years, the trading house’s corporate culture emphasized the independence of business units; as a result, ‘it operated as a confederation of businesses’, according to Prof Goldberg. The confederation has worked to some extent: a diverse business helped to smooth profits. Last year, for example, the industrial businesses provided half the profits, compensating for a lackluster outcome from risk management and financial services. But former and rival executives say the trading house leaves money on the table year after year as it struggles to work together in an integrated way. ‘You still have small fiefdoms within the company,’ says a former executive. Moody’s, the credit rating agency, late last year described Cargill as being ‘challenged to obtain synergies from such a diverse portfolio of businesses’. Mr Page has acknowledged the problem and wants closer ways of working. As an example of the potential, he tells the story of a ‘bond trader, in our proprietary financial desk, [who] saw a security of a big customer of ours get into deep trouble. Rather than just say, “well, that is interesting”, the guy thought: “how do I matter to other people?” ‘So he got hold of the credit manager in one of the businesses he thought could be facing a significant credit risk as a result of something that he was seeing emerging in the trade around this company’s long-term bond. It proved to be true,’ Mr Page adds. ‘The company ended up, four or five months later, bankrupt, but because of his heads-up we averted significant losses.’ In that sense, ‘strategic intent 2015’ is not the kind of revolution that the plan for 2010 created. The change this time is not about moving to new and more lucrative areas of the supply chain but rather, as Mr Page says, to ‘interconnect businesses’. As in the past, Cargill has started by changing its language. While previously it talked about internal collaboration, which had a voluntary aspect, today it speaks of connectivity. ‘What we think will differentiate us over time is this end-to-end awareness connectivity,’ Mr Page says, admitting the change was a response to customers’ concerns: ‘While they were happy to see the direction we were going, there was still an impatience that Cargill did not act cohesively enough in service to their needs.’ As part of its response, the company is hiring from its customers in an effort to understand their needs.”

My colleague, Tom Barnett, also wrote a post about Cargill [A glimpse inside one of the world’s most important companies: Cargill]. In that post, he concluded: “You want to take about a globally integrated enterprise? 138k employees across [67] nations, the hallmark of their vision is, according to CEO Gregory Page, ‘end-to-end awareness connectivity’–as in, don’t just see a supply chain but understand the everything else to which it is connected. Naturally, I admire that kind of thinking when it comes to globalization.” I couldn’t have said it better.