For some time now, I have been predicting that the health of the global economy would rest on the back of an emerging global middle class that increases its consumer spending. One reason is that many markets in developed countries are already saturated and have little room to grow. This is particularly true of in China where household spending remains a small share of the country’s overall economy [“China Inc. Looks Homeward as Americans Buy Less,” by Andrew Batson, Wall Street Journal, 29 September 2009]. Batson writes:

“With the longtime engine of global growth, the American consumer, pummeled by recession, some of China’s hugely productive exporters are eyeing a new market: the Chinese. … ‘China’s ability to consume has now reached a fairly high level. It’s at a turning point,’ says [bicycle manufacturer] Tandem [Industries’] general manager, Tom Tseng. Incomes are rising in China and people can afford more high-quality goods, he says, while ‘in the U.S., people now only want to buy cheap things.’ Chinese businesspeople like Mr. Tseng are adapting to what they believe will be a lasting consequence of America’s deep recession. Savings by suddenly frugal U.S. households soared to an annualized $566 billion in the second quarter, more than quadruple the rate at the start of 2008. While that is important to rebuilding U.S. financial health, it is also sucking demand out of the world economy. China’s exports, after growing for years at a steady 20%-plus rate, recorded a year-over-year drop last November. They kept falling, and in August were down 23% from a year earlier.”

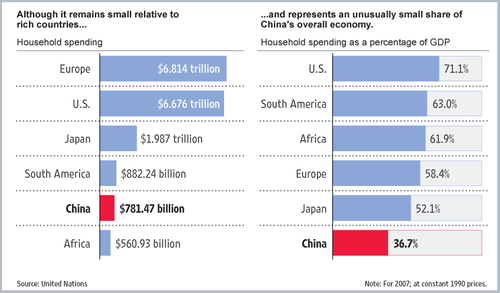

The attached graphic, which accompanied the article, shows why the Chinese market looks so lucrative to manufacturers both in China and elsewhere. Asians (including the Chinese) are well-known for their high savings rates. Government officials and business leaders are hoping that they can coax some of that money out of savings accounts so that it can be spent in the marketplace.

Although spending has dropped and savings increased in America, Batson reports that spending by Chinese consumers “is holding up pretty well, partly because of heavy stimulus spending by a government flush with cash. Urban household spending in China was up 9.2% in the first half of 2009, not far off the country’s average overall growth in recent years.” If Chinese consumer spending increases to the point that it becomes a major portion of the Chinese economy, the demand for goods could cause near-term shortages and rising prices. On the other hand, the world could put excess manufacturing capacity to work along with millions of laid-off workers to meet the demand. According to Batson, however, that may take a few years. The above chart demonstrates why. Right now Chinese consumer spending is closer to that of Africa and South American than it is to either the U.S. or Europe. Despite growing Chinese consumerism, it will take years to become the world’s primary economic engine.

“This shifting dynamic shows how the global economic turmoil is pushing China, the world’s second-largest exporter after Germany, to become a more inward-focused economy. Even once world growth gets back on track, China is likely to run into limits on how much more it can expand its export market share, economists say. The World Bank expects that slower export gains in the future will shave about two percentage points off China’s historical growth rate of 10%. With the recession, Chinese exporters have been taught the dangers of a narrow business model. ‘The lesson we learned from the financial crisis is not to put all your eggs in one basket. We relied too much on the U.S. market,’ says Mr. Tseng, a 42-year-old native of Taiwan. ‘If we had started domestic sales earlier, our business wouldn’t have declined so much this year.’ Chinese domestic demand isn’t a panacea for exporters. For one thing, domestic demand itself can suffer to some extent when exports decline, because the jobs of so many Chinese are linked to export industries. In addition, China’s consumers simply don’t have the money to drive the global economy in the same way as big-spending New Yorkers and Parisians. The consumers of the U.S. and Europe each pump more than $9.5 trillion a year into the global economy, even at their current recession-diminished pace. China’s much poorer households spent in aggregate just over $1.5 trillion last year. Per-capita disposable income in the U.S. was $35,486 in 2008, versus $2,270 in China. So even such a huge and growing country is in no position to replace the U.S. and Europe as an engine of global growth.”

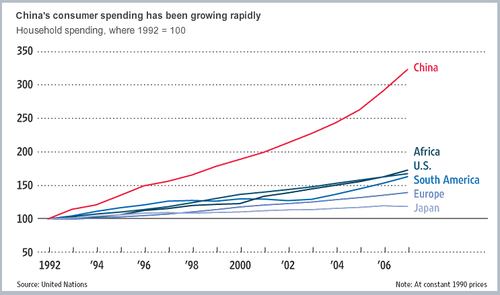

Still, as the below image shows, the rise in Chinese consumer spending is outpacing the rise in consumer spending elsewhere.

The hopes of manufacturers around the world are pinned to that trend. Batson reflects their hopes when he writes, “Asian consumers can help make up the difference and serve as new markets for U.S. companies.” The International Monetary Fund believes that China will lead the world out of the recession [“Can China Lead a Recovery?,” by Steven Mufson, Washington Post, 7 October 2009].

“One year after the global economy went into a tailspin, many economists are wondering whether Chinese consumers, once a thrifty lot, will lead the world out of the recession. Last week, the International Monetary Fund said China would do just that, thanks in part to the government’s $600 billion stimulus package and a flood of bank lending. The IMF increased its forecast of Chinese growth to 8.5 percent in 2009 while lowering its forecast for the U.S. economy, which it said would shrink 2.7 percent. … As a result of the crisis, the U.S. household savings rate has increased to 5 percent from 0 percent, IMF Managing Director Dominique Strauss-Kahn said in a recent interview. While that may be good for global trade and financial balances, he said, it raises the question of which consumers will fill the void and become the new engine of global economic growth. If the most likely candidates are China, India and Brazil, it remains to be seen what kinds of products those consumers will demand, and from whom.”

One reason that manufacturers outside of China are optimistic is that the so-called “China price” is diminishing [“China’s Eroding Advantage,” by Pete Engardio, BusinessWeek, 15 June 2009 print issue]. Engardio notes that “China’s manufacturing advantages remain formidable”; but, even so, “while the total cost of making goods in China was about 5% cheaper than in Mexico three years ago, manufacturing in China now is about 20% more expensive.” According to Batson, that is why “China’s government is increasingly encouraging those exporters that can to look at the domestic market,” To encourage them further, the Chinese government is offering financial incentives. “Domestic subsidies for purchases of cars and home appliances, such as tax breaks and coupons for discounts, have helped boost local sales of those products in recent months.”

China is not the only emerging market being eyed by manufacturers. Other emerging markets are also in their sights [“Corporates: Value of emerging consumers grows clear,” by Richard Milne, Financial Times, 10 September 2009]. Milne writes:

“The financial and economic crises have resulted in a shift eastwards. Robust growth in China and India has drawn the attention of chief executives everywhere, spurred by the deep recessions in much of the developed world. Gerard Kleisterlee, head of one of Europe’s largest companies, Philips, sums it up for many when he says: ‘There will be a structural shift towards Asia and towards China … The demographics already point in that direction of course. By sheer demographics, when [China and India] keep a reasonable pace of growth, they will become the dominant economies of the world. That’s not a reason to despair in what is, today, the developed world. On the contrary, that’s an opportunity for everybody.’ … But companies from the emerging countries themselves which began as low-cost manufacturers for Europe and the US are starting to look closer to home as well. … Underpinning all this is the change in companies from seeing emerging markets as a cheap source of labor and production to places with lots of consumers. … Paul Fletcher, senior partner at Actis, the world’s largest private equity firm specializing in emerging markets. Actis invests from Uganda and Rwanda to Brazil and China. Mr Fletcher says the UK-based company receives similar returns from almost every country. ‘I think there are two main drivers of emerging markets: the emergence of the consumer and the building of infrastructure, both physical and social, in these markets,’ he says. Reaching the consumer in emerging markets also requires companies to invest heavily in research and development locally.”

In my discussions about the Enterra Solutions® Development-in-a-Box™ approach, I have stressed how important it is for developing countries to invest in both infrastructure and people. Mr. Fletcher is seeing the dividends that such investments return. I’ve also noted that innovations developed in response to the needs of the developing world have started making inroads in the developed world as well. In fact, the process is now called “reverse innovation” [“The Joys and Perils of ‘Reverse Innovation,’ BusinessWeek, 5 October 2009 print issue]. All of us will be better off if a robust global middle class emerges. I am hopeful that such a middle class will be more attune to how their spending can affect the environment and will be more responsible than consumers of the past. If they are, then the global economy will set on a much firmer foundation than it has been.

One note of caution, Tony Jackson, a columnist for the Financial Times is concerned that investors won’t weigh all the risks involved in emerging markets [“Emerging markets story symptomatic of wider issue,” 5 October 2009]. Any company looking to do business in an emerging market country would be foolish to rush in without considering all of the risks. Jackson, I believe, is more concerned about people investing in emerging market portfolios than about companies looking to set up businesses. Nevertheless, it’s worth reading what Jackson has to say.

“A senior hedge fund manager claimed the term ’emerging markets’ is now obsolete. They have grown so fast, he wrote in this newspaper, that the distinction between them and developed markets has disappeared. The faster growth of emerging economies is self-evident. The problem with this argument is different, and has to do with risk. For the past five years, the mispricing of risk has bedeviled world markets. Either risk is simply ignored, as in the credit bubble, or investors swing to the opposite extreme in the crunch. The school of thought exemplified by the hedge fund manager seems a clear and slightly worrying case of the former.”

Jackson writes that term “emerging market” has morphed from its original meaning over the years.

“To see why, let us recall what we mean by the term ’emerging market’ in the first place. One political analyst defines it as ‘a country where politics matter at least as much as economics to the markets’. That has nothing to do with either growth or size. One could argue that neither Taiwan nor South Korea are true emerging markets any more, though they are still classed as such. But China and Russia fit the definition admirably. And, as I have remarked in this column before, geopolitical risk is something investors have persistent trouble with. They know it exists, but cannot put a number to it, and thus cannot incorporate it in their models.”

It’s clear from how selectively FDI has been invested in the past that companies understand political risks as well as economic risks — a point also made by Jackson.

“Emerging market indices, dating back to the mid-1980s, have been heavily affected by their country weightings. In the early years, Brazil dominated, then South Korea, and now China. So the story has varied over time.”

Jackson claims that since emerging markets have become open to foreign buyers, “they have raced ahead” except for the period following the 1997 meltdown known as the Asian flu. He just doesn’t know how long that will last. Jackson admits that he is a natural bear and is skeptical of most bullish predictions. For me the bottom line is that companies that invest in emerging markets are helping to reduce the risks by creating jobs and promoting stability. Portfolio investors have no such impact. Not everyone at the Financial Times is as pessimistic as Jackson. David Oakley and Gregory Meyer, for example, write, “For many people the future of investing can be summed up in two words: emerging markets” [“Emerging economies shine in dark times,” Financial Times, 6 October 2009]. They continue:

“During previous bouts of global financial turbulence they have often been harder hit than their developed market counterparts. This time, emerging markets rebounded more quickly, and emerging market assets, particularly equities, have staged far stronger recoveries.”

With room to grow, I continue to believe that emerging market countries present exciting opportunities for businesses looking to expand.