“Blockchain technology stands poised to rewrite how business is conducted if its potential is achieved,” declares Thor Olavsrud (@ThorOlavsrud).[1] But Stefan Thomas (@justmoon), who helped introduce the world to bitcoin, writes, “Blockchains are a pain to work with. Everyone who has done it knows what I’m talking about. The fact that blockchain has been largely ignored by major tech companies and embraced by the financial industry is partly because that industry has a relatively high tolerance for arcane and complex systems.'”[2] Who’s correct? The consensus opinion appears to side with Olavsrud. Nevertheless Thomas’ concerns need to be taken seriously.

Blockchain Challenges

Thomas explains, “At the root of the difficulty in updating blockchains is the need to maintain shared state. In any protocol, everyone has to act the same. But in a blockchain like Ethereum, everyone has to think the same. Everyone’s memory (also known as ‘state’ in computer science terms) has to be exactly the same and evolve according to the same rules. Shared state adds tremendous complexity and that has a big impact on developers.” He goes on to explain that same principle in layman’s terms. “Harmony and consensus are valuable,” Thomas writes. “If we didn’t agree on who is president or how much money is in anyone’s bank account, society would be unable to function.” So what’s the problem? “Harmony taken to the extreme,” Harmon writes, “becomes a detriment.” He then asks, “So how do we find the right balance between too much consensus and too little?” Thomas suggests, in the search for an answer, simplification trumps complexity. He recounts the saga of the emergence of the World Wide Web. Few people know that in the beginning the Web had a rival called Xanadu. “There are many reasons why the Web won in the end,” he writes, “but I believe its stateless architecture was critical to its success. Both Xanadu and the web are decentralized, but the web was much simpler. All it required was a minimal protocol and simple data format.” He continues:

“What can the blockchain industry learn from Xanadu and the world of Web standards? Instead of blindly replacing centralized functions with blockchains, we should be thinking about ways to avoid having those functions be centralized to begin with. We need to build stateless protocols like the Web that can be incrementally improved upon in different corners of the system.”

Matthew Leising explains, “Experimentation and improvements to the software are hampered in a blockchain system because a majority of miners who run the software must agree to deploy the update before it can be rolled out.”[3] Thomas believes by adding “one more layer of abstraction,” blockchain systems could preserve what’s best about blockchain and “and still seamlessly transact with someone who has made different choices.”

Blockchain Advantages

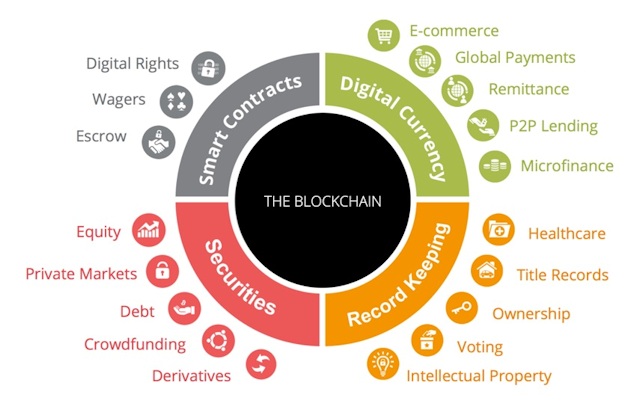

Let’s assume the challenges pointed out by Thomas are eventually overcome and the use of blockchain becomes more ubiquitous. Mark van Rijmenam (@VanRijmenam), Founder of Datafloq, writes, “The possibilities of the Blockchain are enormous and it seems that almost any industry that deals with some sort of transaction, which would mean any industry, can and will be disrupted by the Blockchain. As a result, it is likely that many of these industries will face job losses since intermediaries will be needed a lot less.”[4] BTCS produced the following graphic depicting some potential blockchain applications.

Steve Banker (@steve_scm), Service Director of Supply Chain Management at ARC Advisory Group, believes blockchain technology could revolutionize supply chain applications.[5] He explains how blockchain could work in the supply chain:

“Pallets with RFID tags — or other input devices – would communicate their need to get from point A to point B by a certain date. Carrier ‘mining’ applications would bid for the right to move that load. The RFID tag would award the business to the carrier that bests meets a shipper’s price and service needs. Then as the move progresses, the blockchain would continue to track the shipment. Because the transportation tendering process is analogous to the financial settlement process in Bitcoin, this is a good place to begin exploring the applicability of this technology to the supply chain profession. It is also worth noting that because this uses RFID in a distributed environment that this is also an Internet of Things (IoT) application. Will it work? It is of course too early to say. But if supply chain applications can be built that are truly secure, the benefits would be immense.”

Bob Violino (@BobViolino) reports that International Data Corporation also believes that blockchain has enormous potential in the supply chain arena. He writes, “Blockchain technologies — the technical foundation for Bitcoin — could be key tools for confirming data origin and accuracy, tracking updates and establishing true data authority for millions of different data fields, according to a new study from International Data Corp. (IDC) … According to the new report, blockchain is a solid model for establishing an audit trail, in addition to transferring and monitoring distinct entities that represent items of value. As a result, blockchain has the potential to serve as a foundation for improving the authenticity and accuracy of government records.”[6]

Summary

Admittedly blockchain technology is complex and, maybe, too rigid; but, the upside potential of this technology is enormous. As Ari Juels (@AriJuels), a professor at Cornell Tech, and Dr. Ittay Eyal (@ittayeyal), explain, “The key feature of blockchains is that new data may be written at any time, but can never be changed or erased. At first glance, this etched-in-stone rule seems a needless design restriction. But it gives rise to a permanent, ever-growing transactional history that creates strong transparency and accountability.”[7] In other words, blockchain fosters trust. They add, “Blockchains can be enhanced to support not just transactions, but also pieces of code known as smart contracts. A smart contract is a program that controls assets on the blockchain — anything from cryptocurrency to media rights — in ways that guarantee predictable behavior. A smart contract may be viewed as playing the role of a trusted third party: Whatever task it is programmed to do, it will carry out faithfully.” As noted above, there are challenges that need to be worked out before blockchain becomes the star most pundits believe it will be; but, Irving Wladawsky-Berger, a former IBM executive, believes blockchain will become a star. He writes, “Skeptics needing further reassurance that the Blockchain is truly reaching a tipping point can rest easier with the recent publication of Don Tapscott’s Blockchain Revolution, co-written with his son, Alex. … Build for integrity, power, value, privacy, security, rights and inclusion, they write, and trust will follow.”[8]

Footnotes

[1] Thor Olavsrud, “How Blockchain will Disrupt Your Business,” IT News, 5 September 2016.

[2] Stefan Thomas, “The Subtle Tyranny of Blockchain,” Medium, 18 August 2016.

[3] Matthew Leising, “Man Who Introduced Millions to Bitcoin Says Blockchain Is a Bust,” Information Management, 22 August 2016.

[4] Mark van Rijmenam, “What is the Blockchain and Why is it So Important?” Datafloq, 1 September 2016.

[5] Steve Banker, “Will Blockchain Technology Revolutionize Supply Chain Applications?” Logistics Viewpoints, 20 June 2016.

[6] Bob Violino, “Blockchain Could Be Key Tool For Tracking Data Origin and Authority,” Information Management, 19 May 2016.

[7] Ari Juels and Ittay Eyal, “Blockchains: Focusing on Bitcoin Misses Real Revolution in Digital Trust,” Scientific Computing, 25 July 2016.

[8] Irving Wladawsky-Berger, “Blockchain as ‘Technological Genie’,” The Wall Street Journal, 24 August 2016.