A recent study published by the McKinsey Global Institute indicates that “the rate of return on foreign investment is higher in Africa than in any other developing region” [“What’s driving Africa’s growth?” by Acha Leke, Susan Lund, Charles Roxburgh, and Arend van Wamelen, June 2010]. That might come as a surprise to many people who still view Africa as an economic backwater. Of course, not all nations in Africa are equal. Sweeping statements about the continent do not adequately reflect the variations in economic conditions found amongst Africa states. Nevertheless, the authors of the report recommend that “global executives and investors … pay heed.” They write:

“Africa’s economic pulse has quickened, infusing the continent with a new commercial vibrancy. Real GDP rose by 4.9 percent a year from 2000 through 2008, more than twice its pace in the 1980s and ’90s. Telecommunications, banking, and retailing are flourishing. Construction is booming. Private-investment inflows are surging. To be sure, many of Africa’s 50-plus individual economies face serious challenges, including poverty, disease, and high infant mortality. Yet Africa’s collective GDP, at $1.6 trillion in 2008, is now roughly equal to Brazil’s or Russia’s, and the continent is among the world’s most rapidly growing economic regions. This acceleration is a sign of hard-earned progress and promise.”

Although comparing the African continent’s GDP to Brazil or Russia is interesting, the continent is so big and so diversified that it’s almost an apples and oranges comparison. Still, reporting any good news about the African continent is a refreshing change from the drumbeat of bad news that usually comes from there. The authors continue:

“While Africa’s increased economic momentum is widely recognized, its sources and likely staying power are less understood. Soaring prices for oil, minerals, and other commodities have helped lift GDP since 2000. Forthcoming research from the McKinsey Global Institute (MGI) shows that sources accounted for only about a third of the newfound growth. The rest resulted from internal structural changes that have spurred the broader domestic economy. Wars, natural disasters, or poor government policies could halt or even reverse these gains in any individual country. But in the long term, internal and external trends indicate that Africa’s economic prospects are strong.”

The authors recognize that economies based primarily on extractive industries are subject to market volatility and have dimmer long-term hopes than countries with more diversified economies. As a result, they “developed a framework for understanding how the opportunities and challenges differ by classifying countries according to levels of economic diversification and exports per capita.” They believe their “approach can help guide executives as they devise business strategies and may also provide new insights for policy makers.” That may or may not be true. Analysts don’t have a great track record of predicting the future. If they did, they’d all be billionaires. Nevertheless, conceptual frameworks do have their place as a point of departure for further analysis and discussion. Whether the framework has any predictive value for investors remains to be seen, but I believe the basic assumption (i.e., that diversified economies have better long-term prospects that resource-based economies) is sound. The authors continue:

“To be sure, Africa has benefited from the surge in commodity prices over the past decade. Oil rose from less than $20 a barrel in 1999 to more than $145 in 2008. Prices for minerals, grain, and other raw materials also soared on rising global demand. Yet the commodity boom explains only part of Africa’s broader growth story. Natural resources, and the related government spending they financed, generated just 32 percent of Africa’s GDP growth from 2000 through 2008. The remaining two-thirds came from other sectors, including wholesale and retail, transportation, telecommunications, and manufacturing. Economic growth accelerated across the continent, in 27 of its 30 largest economies. Indeed, countries with and without significant resource exports had similar GDP growth rates. The key reasons behind this growth surge included government action to end armed conflicts, improve macroeconomic conditions, and undertake microeconomic reforms to create a better business climate. To start, several African countries halted their deadly hostilities, creating the political stability necessary to restart economic growth. Next, Africa’s economies grew healthier as governments reduced the average inflation rate from 22 percent in the 1990s to 8 percent after 2000. They trimmed their foreign debt by one-quarter and shrunk their budget deficits by two-thirds. Finally, African governments increasingly adopted policies to energize markets. They privatized state-owned enterprises, increased the openness of trade, lowered corporate taxes, strengthened regulatory and legal systems, and provided critical physical and social infrastructure. Nigeria privatized more than 116 enterprises between 1999 and 2006, for example, and Morocco and Egypt struck free-trade agreements with major export partners. Although the policies of many governments have a long way to go, these important first steps enabled a private business sector to emerge. Together, such structural changes helped fuel an African productivity revolution by helping companies to achieve greater economies of scale, increase investment, and become more competitive. After declining through the 1980s and 1990s, the continent’s productivity started growing again in 2000, averaging 2.7 percent since that year. These productivity gains occurred across countries and sectors. This growth acceleration has started to improve conditions for Africa’s people by reducing the poverty rate. But several measures of health and education have not improved as fast. To lift living standards more broadly, the continent must sustain or increase its recent pace of economic growth.”

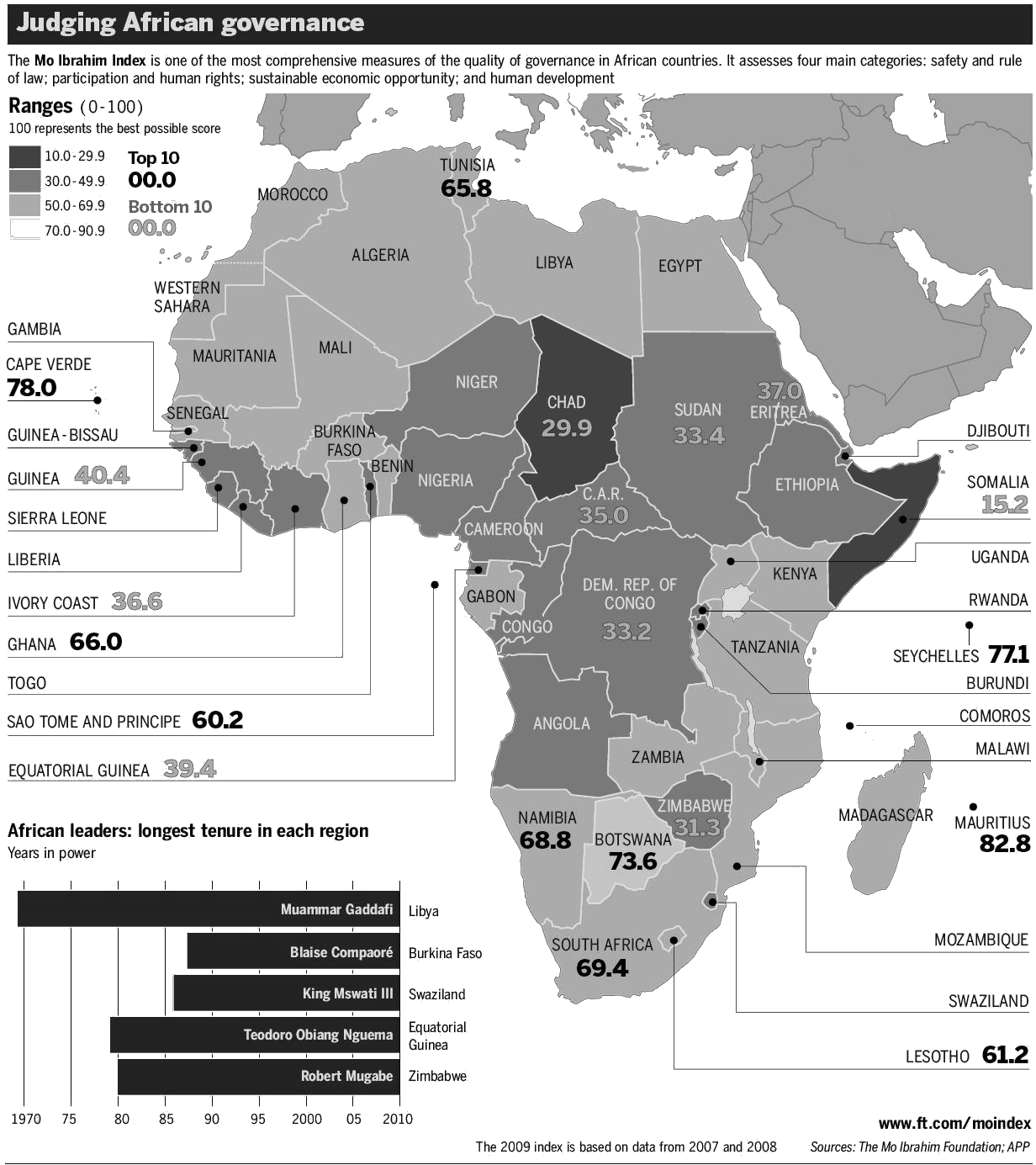

That quick overview of the “good news” about African economies highlights most of the areas that I’ve discussed in past posts about development that require attention from governments (e.g., infrastructure, healthcare, education, and business-friendly policies). One thing it didn’t talk about was governance and corruption, which remain serious anchors to economic growth in many Africa states. As the following Financial Times graphic indicates, most African states have a long way to go in improving governance.

The authors continue their report by exploring “whether Africa’s surge represents a one-time event or an economic take-off.” As I noted above, they recognize that market volatility could result in future “disappointments and setbacks,” but they indicate that their “analysis suggests that Africa has strong long-term growth prospects, propelled both by external trends in the global economy and internal changes in the continent’s societies and economies.” The reason for their optimism is that most African countries are strengthening their connectivity with the global economy; yet, they concede that most of the growth is going to come from continued strong demand for African resources. They explain:

“Although Africa is more than a story about resources, it will continue to profit from rising global demand for oil, natural gas, minerals, food, arable land, and the like. MGI research finds that over the next decade, the world’s liquid-fuel consumption will increase by 25 percent—twice the pace of the 1990s. Projections of demand for many hard minerals show similar growth. Meanwhile, Africa boasts an abundance of riches: 10 percent of the world’s reserves of oil, 40 percent of its gold, and 80 to 90 percent of the chromium and the platinum metal group. Those are just the known reserves; no doubt more lies undiscovered. Demand for commodities is growing fastest in the world’s emerging economies, particularly in Asia and the Middle East. Despite longstanding commercial ties with Europe, Africa now conducts half its trade with developing economic regions (‘South–South’ exchanges). From 1990 through 2008, Asia’s share of African trade doubled, to 28 percent, while Western Europe’s portion shrank, to 28 percent, from 51 percent. This geographic shift has given rise to new forms of economic relationships, in which governments strike multiple long-term deals at once. China, for example, has bid for access to ten million tons of copper and two million tons of cobalt in the Democratic Republic of the Congo in exchange for a $6 billion package of infrastructure investments, including mine improvements, roads, rail, hospitals, and schools. India, Brazil, and Middle East economies are also forging new broad-based investment partnerships in Africa.”

For more on these “South-South exchanges,” read my post entitled South to South Relationships begin to Strengthen. The authors believe that increased demand for resources has given “African governments more bargaining power, so they are negotiating better deals that capture more value from their resources.” Questions remain as to who is profiting from that value — national treasuries or corrupt politicians and their cronies. The authors of the study next broach a subject that is critical for sustained economic growth: foreign direct investment. They write:

“Africa is gaining increased access to international capital. The annual flow of foreign direct investment into Africa increased from $9 billion in 2000 to $62 billion in 2008—relative to GDP, almost as large as the flow into China. While Africa’s resource sectors have drawn the most new foreign capital, it has also flowed into tourism, textiles, construction, banking, and telecommunications, as well as a broad range of countries.”

As noted above, much of this investment is coming from China. As I’ve noted in previous posts, however, countries are learning that Chinese investments are often accompanied by a large number of Chinese workers who fill jobs that local leaders were hoping would be made available to indigenous workers. In fairness, the influx of money has brought with it some jobs, just not as many as hoped for. As a result of those new jobs, many African states are seeing an emerging consumer base and that base is another reason that the study’s authors are optimistic about Africa’s future. They continue:

“Africa’s long-term growth will increasingly reflect interrelated social and demographic changes creating new domestic engines of growth. Key among these will be urbanization, an expanding labor force, and the rise of the middle-class African consumer. In 1980, just 28 percent of Africans lived in cities. Today, 40 percent of the continent’s one billion people do—a proportion roughly comparable to China’s and larger than India’s. By 2030, that share is projected to rise to 50 percent, and Africa’s top 18 cities will have a combined spending power of $1.3 trillion.”

Population growth in Africa is also seen by the authors as a positive thing. They explain:

“Africa’s labor force is expanding, in contrast to what’s happening in much of the rest of the world. The continent has more than 500 million people of working age. By 2040, their number is projected to exceed 1.1 billion—more than in China or India—lifting GDP growth. Over the last 20 years, three-quarters of the continent’s increase in GDP per capita came from an expanding workforce, the rest from higher labor productivity. If Africa can provide its young people with the education and skills they need, this large workforce could become a significant source of rising global consumption and production. Education is a major challenge, so educating Africa’s young has to be one of the highest priorities for public policy across the continent.”

Providing education and training for Africa’s youth will not be easy. If they don’t receive the skills necessary to attract employers, then Africa’s burgeoning population will be a drawback rather than an advantage. The authors are betting that Africans will get jobs and that those jobs will foster the emergence of a middle class. They continue:

“Many Africans are joining the ranks of the world’s consumers. In 2000, roughly 59 million households on the continent had $5,000 or more in income—above which they start spending roughly half of it on nonfood items. By 2014, the number of such households could reach 106 million. Africa already has more middle-class households (defined as those with incomes of $20,000 or above) than India. Africa’s rising consumption will create more demand for local products, sparking a cycle of increasing domestic growth.”

The authors eventually explain how their framework differs from traditional taxonomies that group African countries “by region, language, or income level.” Their framework classifies “26 of the continent’s largest countries according to their levels of economic diversification and exports per capita.” They explain:

“This approach highlights progress toward two related objectives:

- Diversifying the economy. In the shift from agrarian to urban economies, multiple sectors contribute to growth. The share of GDP contributed by agriculture and natural resources shrinks with the expansion of the manufacturing and service sectors, which create jobs and lift incomes, raising domestic demand. On average, each 15 percent increase in manufacturing and services as a portion of GDP is associated with a doubling of income per capita.

Boosting exports to finance investment. Emerging markets require large investments to build a modern economy’s infrastructure. Exports are the primary means to earn the hard currency for imported capital goods, which in Africa amount to roughly half of all investment. This is not to say that African countries must follow an Asian model of export-led growth and trade surpluses, but they do need exports to finance the investments required to diversify.

History shows that as countries develop, they move closer to achieving both of these objectives. Most African countries today fall into one of four broad clusters: diversified economies, oil exporters, transition economies, or pretransition economies. Although the countries within each segment differ in many ways, their economic structures share broad similarities. Our framework is useful for understanding how growth opportunities and challenges vary across a heterogeneous continent. Although imperfect, this framework can guide business leaders and investors as they develop strategies for Africa and can provide new perspectives for its policy makers.”

The authors then provide some details about each of these groupings of states beginning states they have classified as having diversified economies.

“The continent’s four most advanced economies—Egypt, Morocco, South Africa, and Tunisia—are already broadly diversified. Manufacturing and services together total 83 percent of their combined GDP. Domestic services, such as construction, banking, telecom, and retailing, have accounted for more than 70 percent of their growth since 2000. They are among the continent’s richest economies and have the least volatile GDP growth. With all the necessary ingredients for further expansion, they stand to benefit greatly from increasing ties to the global economy. Domestic consumption is the largest contributor to growth in these countries. Their cities added more than ten million people in the last decade, real consumer spending has grown by 3 to 5 percent annually since 2000, and 90 percent of all house-holds have some discretionary income. As a result, consumer-facing sectors such as retailing, banking, and telecom have grown rapidly. Urbanization has also prompted a construction boom that created 20 to 40 percent of all jobs over the past decade.”

The authors indicate that these countries still face some challenges, like “continuing to expand exports while building a dynamic domestic economy” in light of the fact that they have “unit labor costs (wages divided by output per worker) two to four times higher than those in China and India.” As a result, these countries need to “move toward producing higher-value goods.” The fact that the so-called China Price is rising, will make them more competitive with goods coming from there (see my post entitled The “China Price” Continues to Rise). Egypt and Libya still face significant political challenges as succession worries cloud the future (see my post on Libya entitled The Letdown in Libya). The authors next turn to countries they classify as oil exporters:

“Africa’s oil and gas exporters have the continent’s highest GDP per capita but also the least diversified economies. This group—Algeria, Angola, Chad, Congo, Equatorial Guinea, Gabon, Libya, and Nigeria—comprises both countries that have exported oil for many years and some relative newcomers. Rising oil prices have lifted their export revenues significantly; the three largest producers (Algeria, Angola, Nigeria) earned $1 trillion from petroleum exports from 2000 through 2008, compared with just $300 billion in the 1990s. For the most part, Africa’s oil and gas exporters used this revenue well, to reduce budget deficits, fund investments, and build foreign-exchange reserves. Economic growth in these countries remains closely linked to oil and gas prices. Manufacturing and services account for just one-third of GDP—less than half their share in the diversified economies. The experience of emerging-market oil exporters outside Africa illustrates the potential for greater diversification. In Indonesia, manufacturing and services account for 70 percent of GDP, compared with less than 45 percent in Algeria and Nigeria—even though all three countries have produced similar quantities of oil since 1970. … The oil exporters generally have strong growth prospects if they can use petroleum wealth to finance the broader development of their economies. The experience of other developing countries shows it will be essential to make continued investments in infrastructure and education and to undertake further economic reforms that would spur a dynamic business sector. But like petroleum-rich countries in general, those in Africa face acute challenges in maintaining political momentum for reforms, resisting the temptation to overinvest (particularly in the resource sector), and maintaining political stability—in short, avoiding the ‘oil curse’ that has afflicted other oil exporters around the world.”

African nations have not done well at avoiding the oil curse. In fact, Nigeria is probably the poster child for the curse. With a number of analysts now predicting peak oil to be reached within the next decade (admittedly a prediction that has been erringly made before), time seems to be running out for countries to gain maximum benefit from their oil resources. The authors next turn to states that have been classified as having transition economies:

“Africa’s transition economies—Cameroon, Ghana, Kenya, Mozambique, Senegal, Tanzania, Uganda, and Zambia—have lower GDP per capita than the countries in the first two groups but have begun the process of diversifying their sources of growth. These countries are diverse: some depend heavily on one commodity, such as copper in Zambia or aluminum in Mozambique. Others, like Kenya and Uganda, are already more diversified. The agriculture and resource sectors together account for as much as 35 percent of GDP in the transition countries and for two-thirds of their exports. But they increasingly export manufactured goods, particularly to other African countries. Successful products include processed fuels, processed food, chemicals, apparel, and cosmetics. As these countries diversified, their annual real GDP growth accelerated from 3.6 percent a year in the 1990s to 5.5 percent after 2000. Expanding intra-African trade will be one key to the future growth of the transition economies, because they are small individually, but their prospects improve as regional integration creates larger markets. If these countries improved their infrastructure and regulatory systems, they could also compete globally with other low-cost emerging economies. One study found that factories in the transition countries are as productive as those in China and India but that the Africans’ overall costs are higher because of poor infrastructure and regulation—problems that the right policy reforms could fix. The local service sectors (such as telecommunications, banking, and retailing) in the transition economies also have potential. While they are expanding rapidly, their penetration rates remain far lower than those in the diversified countries, creating an opportunity for businesses to satisfy the unmet demand.”

Countries in East Africa are trying to work together to create a diversified economic region (see my post entitled The Plight and Hope of East Africa. The authors next look at countries they classify as having pretransition economies:

“The economies in the pretransition segment—the Democratic Republic of the Congo, Ethiopia, Mali, and Sierra Leone—are still very poor, with GDP per capita of just $353—one-tenth that of the diversified countries. Some, such as Ethiopia and Mali, have meager commodity endowments and large rural populations. Others, devastated by wars in the 1990s, started growing again after the conflicts ended. But many pretransition economies are now growing very fast. The three largest (the Democratic Republic of the Congo, Ethiopia, and Mali) grew, on average, by 7 percent a year since 2000, after not expanding at all in the 1990s. Even so, their growth has been erratic at times and could falter again. Although the individual circumstances of the pre-transition economies differ greatly, their common problem is a lack of the basics, such as strong, stable governments and other public institutions, good macroeconomic conditions, and sustainable agricultural development. The key challenges for this group will include maintaining the peace, upholding the rule of law, getting the economic fundamentals right, and creating a more predictable business environment. These countries can also hasten their progress with support from international agencies and new private philanthropic organizations that are developing novel ways to tackle poverty and other social issues. In a more stable political and economic environment, some of these countries could tap their natural resources to finance economic growth. The Democratic Republic of the Congo, for example, controls half of the world’s cobalt reserves and a quarter of the world’s diamond reserves. Sierra Leone has about 5 percent of the world’s diamond reserves. Ethiopia and Mali have 22 million and 19 million hectares of arable land, respectively. If these countries could attract businesses to help develop their resources, they could push their economies upward on the path of steadier growth.”

As I have repeatedly asserted, economic development and security go hand-in-hand. Most of these pretransition economies suffer from a lack of security which adversely affects their economic prospects. Although there is some hope for a better future in these countries, at the moment it is a dim hope. The authors conclude:

“If recent trends continue, Africa will play an increasingly important role in the global economy. By 2040, it will be home to one in five of the planet’s young people, and the size of its labor force will top China’s. Africa has almost 60 percent of the world’s uncultivated arable land and a large share of the natural resources. Its consumer-facing sectors are growing two to three times faster than those in the OECD countries. And the rate of return on foreign investment is higher in Africa than in any other developing region. Global executives and investors cannot afford to ignore this. A strategy for Africa must be part of their long-term planning. The time for businesses to act on those plans is now. Companies already operating in Africa should consider expanding. For others still on the sidelines, early entry into emerging economies provides opportunities to create markets, establish brands, shape industry structures, influence customer preferences, and establish longterm relationships. Business can help build the Africa of the future. And working together, business, governments, and civil society can confront the continent’s many challenges and lift the living standards of its people.”

I agree that Africa has great potential; but it’s always had great potential. Lack of good governance and pervasive corruption have prevented that potential from being achieved. If governance is not improved and corruption is not curtailed, Africa’s future prospects look worse not better. As an optimist, however, I look at the organizations working persistently to improve Africa and have to believe that Africans themselves will eventually overcome a ubiquitous tribal mentality to embrace grassroots efforts that will forever transform Africa’s political landscape. Such transformations may never happen in places like Somalia or other states cursed with armed extremist religious groups, but many African states I believe will achieve their potential. As authors of the McKinsey study conclude, that effort will take the combined efforts of people from government, business, and non-governmental organizations as well as individual citizens. The road will be difficult and pitted with challenges, but the effort it will take to travel down it will be worth the journey.