Mar 18, 2015

Steve

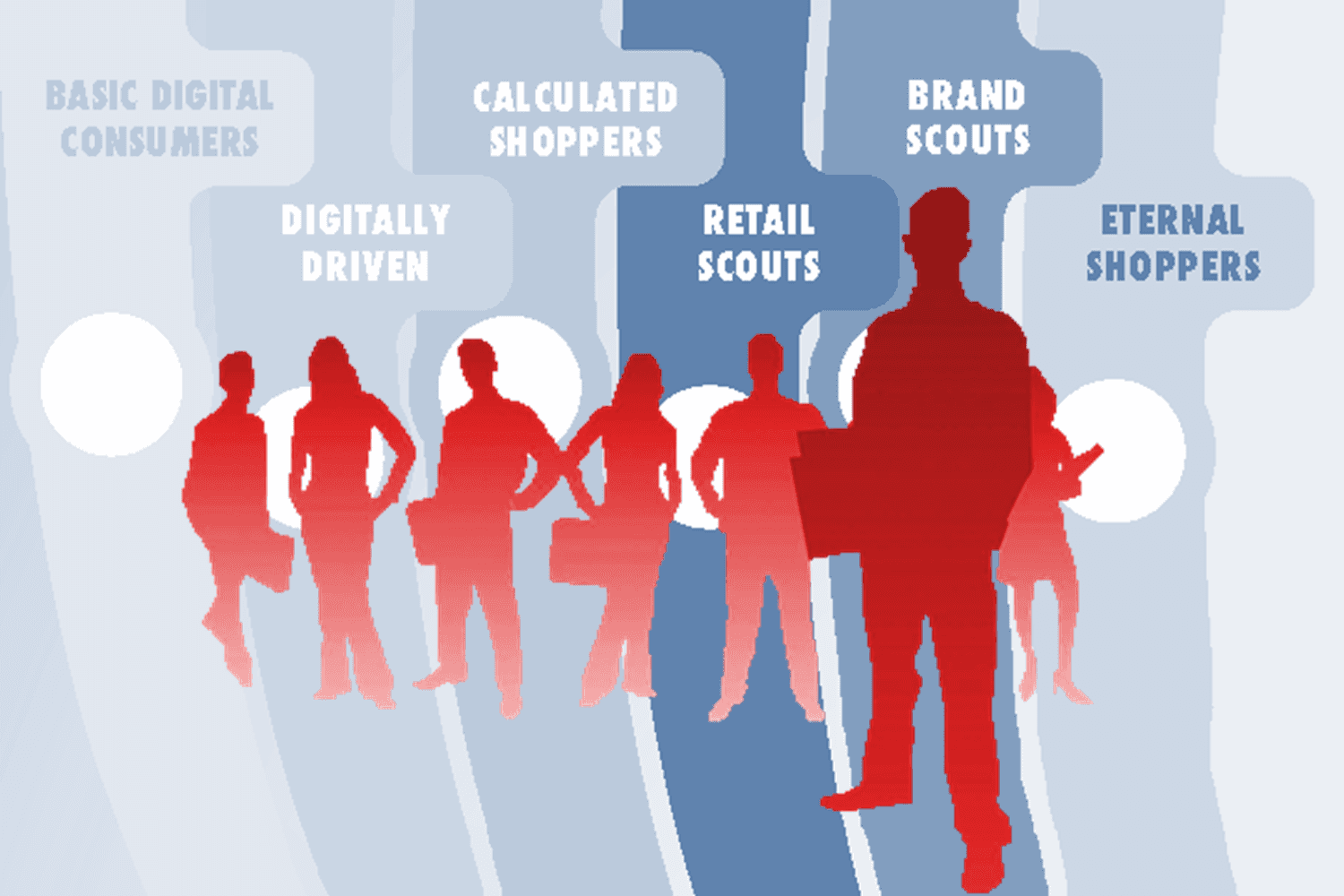

In a masterful bit of understatement, the folks at Google note, "These days, the customer journey has grown more complex." In trying to describe this new customer journey, you hear terms like "multi-channel," "omnichannel," and "digital path to purchase" (DP2P). In today's business world, digital technologies will more than likely play some role in a customer's decision to purchase a product or service. Although the term "digital path to purchase" implies there is a single path consumers follow on their journey to buying something, that's simply not the case. The paths used by consumers are often unique to individuals. Tyson Goodridge (@goodridge), a marketing contractor for Compete, notes that a study released a couple of years ago by GroupMNext and Compete, tried to simplify the discussion by grouping digital consumers into six groups.[1] According to the study, these groups contain "consumers who utilized digital at least once in their purchase pathway. The segments are:

Basic Digital Consumers: These are not highly digital users. They are comfortable with Internet shopping and research, but they are not mobile or social and have the second-highest likelihood of buying offline.

Retail Scouts: These consumers have short journeys and prefer retail sites to brand sites. They use mobile, but are twice as likely to use it in the home as out. They are comfortable buying online but did not express a preference between online and offline.

Brand Scouts: Brand Scouts are the spiritual partner to the Retail Scouts except instead of having a favorite retailer, they have a favorite brand. When asked, 72% said they start their journey with a brand in mind.

Digitally Driven Segment: They use every digital tool at their disposal. They use social and mobile more than any other segment in the study, value convenience above all else and they do everything in their power to avoid physically going to a store. The Digitally Driven exist in good numbers already, but within five years this will be the dominant segment of consumers.

Calculated Shoppers: These shoppers seem to know they are going to make a purchase, but they are deciding which brand to choose. They are similar to the Digitally Driven Segment, but have no urgency to their purchase and they’re willing to take the time to get the best deal.

External Shoppers: These are non-mobile shoppers. They want the answers to, 'Should I buy?', 'What do I buy?' and 'What brand do I buy?' — all at the same time. These shoppers have no urgency to make a purchase and they do their research on desktop and laptop computers.

An AOL Advertising study looked at the DP2P picture from a technology rather than a consumer perspective and examined six digital channels used by consumers. Those channels are: affiliate, social, email, display, non-brand search, and brand search. According to the MarketingCharts staff, "The study finds that each [digital channel sees] a majority share of [its] impact come in the 'middle' of the conversion path."[2] The staff elaborates:

"Even so, there are significant discrepancies in the impact each has at different points:

Display and social are the most likely to serve as a middle touchpoint, mirroring results from a similar Google study;

Brand and non-brand search are the channels most likely to be used as the only touch points in a sales conversion;

Affiliate and brand search are weighted more towards a last-touch impact than any other channel analyzed; and

Brand and non-brand search have more of a first-touch impact than the other channels.

In short, display and social tend to be used most during the awareness and consideration stage, brand search is skewed more towards the initial stage than other channels, and the affiliate channels is tilted more towards the last point of the funnel than the other channels."

At the simplest level, you could put the consumer types and the digital channels into a 6X6 matrix to get an idea about how complex the digital path to purchase has become (and why the imagery of simple "path" is inadequate to depict what is really going on). Eric Hazan (@eric5555), a principal with McKinsey & Company, notes that you can add another layer of complexity into your analysis by examining the various phases that consumers go through on their path to purchase. "Marketers have long recognized that a purchase is far more than a solitary event when the actual financial transaction between shopper and retailer takes place," Hazan writes. "This is just one point along the very nuanced consumer decision journey (CDJ). Each stage of the journey might be experienced in a matter of moments or could take years to complete."[3] Hazan continues:

Regardless of the duration, the journey usually spans five phases:

1. Consideration. Consumers assemble an initial set of brands and retailers to consider. 2. Evaluation. The consideration set evolves and preferences emerge as the shopper gathers information from a variety of online and offline sources. 3. Purchase. The shopper selects what to buy, where to buy it, and how to take delivery. 4. Experience. The new product owner reacts to the purchase and interacts with the product and brand. 5. Loyalty. After owning the product, consumers decide whether or not to select the same product or brand again.

All this talk about the digital path to purchase might lead one to believe that eCommerce is now the dominant retail sector. That's simply not true. Rich Sherman, author and founder at Gold & Domas Research, notes that eCommerce is "still only 6 percent of total U.S. retail spend."[4] That means that most of the "digital" part of the path involves decision making rather than conversion. Sherman goes on to make an important point about the digital path to purchase by distinguishing between eCommerce and mobile commerce. He explains, "Consumer ecommerce is being supplanted by mobile commerce with shoppers using their smartphone before and during the offline shopping experience." In the coming years, the smartphone will play an even more important role in the digital path to purchase. "Smartphones matter partly because of their ubiquity. They have become the fastest-selling gadgets in history, outstripping the growth of the simple mobile phones that preceded them. They outsell personal computers four to one. Today about half the adult population owns a smartphone; by 2020, 80% will."[5] With 80% of adult consumers having access to smartphone technology in the years ahead, successful businesses must have a winning digital strategy. Tricia Nichols, Managing Partner at MediaCom US, puts it this way, "The unstoppable march of digital marketing is forcing retail brands to fundamentally transform their relationships with shoppers."[6] Sherman adds, "Savvy brands will use new 'point of demand' information illuminating the path to purchase through promotions and to develop more accurate demand/supply plans to sense, shape and respond to demand variability. Technologies that support tactical simulations, provide predictive/prescriptive analytics, and enable collaboration are requirements to stay in the game."

Footnotes [1] Tyson Goodridge, "The 6 Types of Digital Consumers and Their Paths to Purchase," Compete Pulse, 30 May 2013. [2] Staff, "Where Do Digital Channels Have Most of Their Impact on the Path to Purchase?," MarketingCharts, 8 September 2014. [3] Eric Hazan, "The multichannel journey: Profitably shaping the path to purchase," McKinsey on Marketing and Sales, March 2014. [4] Rich Sherman, "Is Your 'Path to Purchase' a Trail or Superhighway?" SupplyChainBrain, 24 February 2015. [5] Staff, "Planet of the phones," The Economist, 28 February 2015. [6] Tricia Nichols, "Digital Retailers' New Path to Purchase," Mediacom, 29 November 2011.