The Business Continuity Institute, a UK-based organization that was established “to promote the art and science of business continuity management and to assist organisations in preparing for and surviving minor and large-scale man-made and natural disasters,” recently released a survey that concludes “the sources of supply chain failure are deeply rooted.” [“Supply Chains Need to Be More Resilient as Disruptions Are Widespread, Survey Finds,” SupplyChainBrain, 9 November 2011] According to the article, “Respondents from 62 countries revealed that 85 percent of organisations recorded at least one supply chain disruption in 2011 with 40 percent of analysed disruption originating below the immediate supplier.” The survey’s results further highlight the need for more supply chain visibility. Supply chain analyst Lora Cecere has recommended that, at a minimum, visibility should be pursued from a supplier’s supplier to a customer’s customer. The article continues:

“The survey, now in its third year, emphasises the need for a higher priority to be assigned to developing resilient supply chains in the face of systemic vulnerabilities and unpredictable disruptive events. Supply chain and business continuity management techniques are available and offer the opportunity to better understand supply chain continuity risk and provide methods for managing continuity of key supply chains. … The survey report concludes that effectively managing supply chain continuity is critical not just because of the immediate costs of disruption, but also the longer term consequences to stakeholder confidence and reputation that may arise following a supply chain failure.”

That conclusion is certainly not new or surprising. Apparently, however, companies need to be continually reminded that supply chain resiliency is a serious matter. Other findings from the survey include:

• 51% cited adverse weather as being the main cause of disruption, maintaining its prominence from the 2010 report. Unplanned IT and telecommunication outages were the second most likely disruption, affecting 41%.

• Cyber attack has risen to become a top three source of disruption in the financial services sector.

• Supply chain incidents led to a loss of productivity for almost half of businesses along with increased cost of working (38%) and loss of revenue (32%).

• Longer term consequences of disruption in the supply chain included shareholder concern (19%), damage to reputation (17%), and expected increases in regulatory scrutiny (11%).

• The earthquakes and tsunami experienced in Japan and New Zealand this year, affected 20% of responding organisations, which were headquartered in 18 countries and 12 industry sectors.

• For 17% of respondents the financial costs of the largest single incident totaled a million or more Euros. This figure almost doubles to 32% where less resilient supply chains are evident in the research.

As supply chains have become extended, their complexity and their exposure to risks have increased. The survey was conducted prior to the flooding in Thailand which may have increased respondent exposure to disruption. The point is that events that were once considered black swans are no longer uncommon. Companies that fail to have robust contingency and business continuity plans are going to continue to suffer the consequences of aperiodic disruptions. The article concludes:

“Lyndon Bird, technical director at the institute, commented: ‘While just-in-time efficiencies and outsourcing strategies are here to stay in some form, this survey shows it is more critical than ever to strike a sensible balance between the need to drive down costs and the need for these cost savings not to be wiped out through disruption or unacceptable risk exposure, especially in the context of the longer term reputational damage. Business continuity management can help in gaining a better understanding of likely supply chain behaviour when faced by disruption and help build confidence in an effective response and continuity of supply.'”

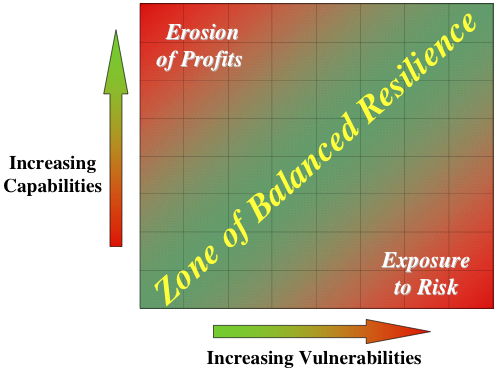

Time and again the issue of balance between “lean” and “resilient” supply chains is raised by risk management experts. In his doctoral dissertation entitled Supply Chain Resilience: Development of a Conceptual Framework, an Assessment Tool and an Implementation Process, Timothy J. Pettit, included a graphic that, in a very general way, illustrated why balance is the key.

Pettit’s point is that resiliency does come with a price that can erode profits. A lack of resiliency, however, can also affect profits and even expose a company to total failure. Hence, finding what Pettit calls the “Zone of Balanced Resilience” is essential. In his abstract, Pettit writes, “The business environment is always changing and change creates risk. Managing the risk of the uncertain future is a challenge that requires resilience – the ability to survive, adapt and grow in the face of turbulent change. … Findings suggest that supply chain resilience can be assessed in terms of two dimensions: vulnerabilities and capabilities.” As a result of his research, he “identified seven vulnerability factors composed of 40 specific attributes and 14 capability factors from 71 attributes that facilitate the measurement of resilience.” Much of the focus of his dissertation deals with an assessment tool that was developed at the university he was attending. He explains:

“The Center for Resilience at The Ohio State University (OSU) has developed a new supply chain resilience framework to assist businesses deal with change: resilience is ‘the ability of an enterprise to survive, adapt and grow in the face of change and uncertainty.’ We created a tool for measuring resilience in a business enterprise – Supply Chain Resilience Assessment & Management (SCRAM™) – to assess supply chain resilience in terms of two major dimensions:

• Vulnerabilities – fundamental factors that make an enterprise susceptible to disruptions

• Capabilities – attributes that enable an enterprise to anticipate and overcome disruptions

“We define the Zone of Balanced Resilience as a balance between vulnerabilities and capabilities, where firms will be the most profitable in the long term.”

If you want to read more about how uncertainty can affect the supply chain, read my post entitled Uncertainty, Confidence, and Catch-22 in the Supply Chain. Pettit concludes:

“Although further validation is required, managers should be encouraged to make the minimal investment required to determine their current state of resilience and compare their strategy with the resilience fitness space.”

If you’re interested, you should download and read Pettit’s entire dissertation. Robert J. Bowman, Managing Editor of SupplyChainBrain, also believes that making an assessment of your capabilities is a good idea. “Some kind of early-warning system for supplier stability,” he writes, “is essential – now more than ever. When it comes to the solidity of the typical supplier base, retailers and original equipment manufacturers these days are skating along on thin ice.” [“Do You Have a Stable Supplier Base? Are You Sure About That?” 18 April 2011] According to Bowman, one of the reasons that the ice has been thinned is because so many companies have adopted lean practices. He writes:

“To cut costs, they’ve consolidated vendors down to the barest minimum – sometimes just one for a given component or region. That’s a fine way to boost buying leverage, but it also raises the risk of a major supply-chain disruption in the event of natural or economic disaster. The kind of thing that seems to happen every other week. Making matters worse are the stretched-out lead times caused by outsourcing to Asia and other locations far from end markets. Companies that crossed the ocean in search of cheap labor are discovering how much tougher it is to solder a snapped link in the chain.”

The primary focus of Bowman’s article is on suppliers that are fiscally unsound and at risk of failing. He writes:

“So how can manufacturers do a better job of detecting future failures among their suppliers? Start by realizing the limitations of traditional financial data. ‘It’s one of the easiest things to [examine] – and the one that lets everybody down the most,’ says Jon Bovit, chief marketing officer with CVM Solutions. And when you do request a supplier’s financial statement, don’t stop with one. The best practice, he says, is to demand three years’ worth of financials and credit reports on a rolling basis. That’s essential information, but it can be misleading. By the time bad news creeps into a financial report, it’s often too late. Risk scores based on periodic statements provide a snapshot of the company’s health several months or quarters ago. ‘They don’t give you a very forward-looking perspective,’ Bovit says. … Bovit recommends supplementing financials with a ‘usage trust metric.’ Simply put, that’s a measure of whether a supplier is losing or gaining customers.”

Bovit told Bowman that he also recommends listening to the “chatter” about suppliers that can be found on social networks.

“Social networks are an excellent place to get a sense of what companies are saying about their vendors. ‘If there seems to be a lot of pure news counts on a certain supplier you have in Japan, chances are it’s being affected,’ says Bovit. Internal communications within a large buying organization can also reveal weaknesses within the supply base. It helps to know what the person in the next cubicle is talking about.”

Although Bowman recommends that companies be pro-active in assessing their supply chains, he admits that one strategy is doing “nothing to assess the health of your suppliers, then count on your ability to adjust quickly when one or more of them goes belly up.” Josh Green, chief executive officer of Panjiva, told Bowman, “That’s actually not a crazy strategy.” He explains, “It’s reasonable if you have a nimble organization.” In retort, Bowman asks, “Do you really want to take that chance?” He continues:

“There are too many stories about ‘best-in-class’ manufacturers who suffered serious supply-chain crises after an economic slump or even a factory fire caused by lightning. The problem with traditional [financial] risk-management tools, says Green, is that they weren’t designed for the supply chain. They were created by credit-rating agencies to evaluate customers, not suppliers. And they’re most effective when the user has access to a wealth of financial data about the company it’s investigating, which isn’t always the case with suppliers based outside the U.S.”

Green also told Bowman that he recommends that companies go beyond investigating their immediate suppliers. They should “find out the identity of the supplier’s suppliers, so you can track whether it’s paying its bills on time.” Bowman does acknowledge that there are “other kinds of supply failures have nothing to do with financial distress.” He concludes:

“A key vendor might drop you as a customer, in favor of a more lucrative competitor. Such a scenario ‘has not even remotely been touched by traditional financial measures,’ says Green. There’s also the possibility of severe damage to one’s brand by irresponsible behavior on the part of the supplier, in the form of tainted products. One metric isn’t going to tell the whole story – not by a long shot. ‘When the Great Recession got going, all of a sudden it was all about risk,’ says Green. ‘Amazingly enough, two years on, there still is nothing even approaching a silver bullet when it comes to supplier risk management.’ But smart companies aren’t without ammunition.”

Green’s assessment certainly substantiates the conclusion of the Business Continuity Institute survey that “the sources of supply chain failure are deeply rooted.” That being the case, finding Pettit’s “Zone of Balanced Resilience” makes a lot of sense if you want your company to thrive in the years ahead.