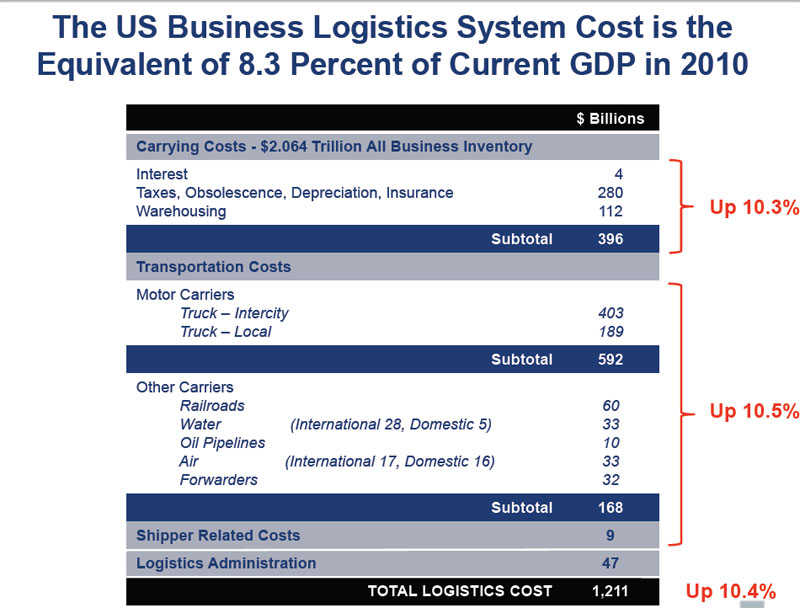

A year ago the folks at Supply Chain Digest reported the findings of “the State of the Freight Report from the newly renamed Wolfe, Trahan & Co. (formerly Wolfe Research)” in which analysts predicted that, during the period between June of last year and June of this year, supply chain transportation costs would rise at an annualized rate of “5.3% (that would include both volume, rate and fuel surcharge increases).” [“Mood Starts to Shift as Shippers Expect Freight Rate Increases, Capacity to Tighten, according to Latest State of the Freight Report,” 7 June 2010]. The predicted rise in freight charges were expected to be the result of rising demand and limited capacity. Analysts predicted “the highest rate increases” would be found in “ocean shipping, with global airfreight, truckload carriage and regular rail all not far behind.” As the following chart shows, the State of the Freight report was right about the increases but wrong about the rate. Transportation costs nearly doubled the prediction.

Source: “Breakdown of 2010 US Logistics Costs,” Supply Chain Digest, 16 June 2011.

A survey of industry leaders conducted at the beginning of this year, identified “cost, service and finding adequate transportation capacity as continuing priorities.” [“Rising Transportation Costs in 2011,” by Ted Schaefer, Supply Chain Digest, 10 February 2011]. Schaefer reported that the Council of Supply Chain Management Professionals (CSCMP) claims that “63% of the total logistics costs” are tied up in transportation. According to Dave Howland, vice president of land transportation services at APL Logistics, freight capacity is likely to remain tight in the years ahead. [“The Capacity Crunch: What’s Ahead,” SupplyChainBrain, 12 August 2011]. He explains why:

“Ocean and land carriers that pared down their fleets during the 2008-2009 recession are being very cautious about adding back capacity. … Couple that with new truck safety regulations expected to further shrink the driver pool and it becomes clear that capacity shortages will be a fact of life for several years to come.”

Matthew Menner, senior vice president of Transplace, claims that “the right IT solutions are helping the industry deal with” transportation challenges (including new motor carrier safety regulations and rising oil prices). [“Attacking Transportation Challenges in the Retail Supply Chain,” SupplyChainBrain, 27 June 2011] “Forward looking shippers are rethinking their sourcing strategies, developing longer-term contracts with transportation providers and taking other steps to be prepared for changing market dynamics, he says.” Apparently, however, there are fewer “forward thinking shippers” than you might imagine. Schaefer examined CSCMP’s most recent release of its Annual State of Logistics Report and discovered a few “intriguing findings.” He explains:

“First, we were quite surprised to find that one out of every four respondents was unable to confirm whether or not their most recent improvement projects in the transportation arena had any impact. Wow! We don’t envy those managers walking into their bosses’ offices trying to explain that their project ‘might have worked, but then again, it might not.’ The ability to measure what’s going on in your transportation network is a prerequisite for improvement. Once again, we observe the fact that the computerization of the supply chain doesn’t always yield more information. Someone has to know that to collect and how to put it together before it can be useful.”

People in the intelligence community have insisted for years that in order for information to be useful it must be actionable. The bottom line for any supply chain analytics system should be that it is able to turn data into actionable information. Schaefer continues:

“The second intriguing finding in this year’s survey was that only 30% of respondents had been out in the market with a bid over the previous 12 months. With all of the change in the marketplace as carriers consolidate, remove capacity or go out of business we were surprised that so few shippers were out in the market forging agreements for capacity and making sure their rates were competitive.”

To use a sports metaphor to explain Schaefer’s concern, you can’t change the outcome of the game if you’re not playing. Schaefer’s final observation is about transportation management. He writes:

“Finally, 75% of our survey respondents continue to struggle with the trade-off between adding carriers to reduce costs and limiting the total number of carriers so they can be effectively managed for service and other improvements. With the number of different software packages and service providers in the market today that can explicitly quantify this trade-off in their bid optimization packages, there is clearly an opportunity to eliminate this struggle for most of these shippers.”

In other words, Schaefer agrees with Menner that that “the right IT solutions” can help the industry deal with transportation challenges. Schaefer concludes:

“After reviewing the survey results, we continue to advise our clients to hold someone in the organization accountable to know what they spend on freight, where they spend it and why they spend it. This also means providing them with the means to measure the spend as well the resources and tools to stay close to the market and manage not only the spend, but the relationships with the carriers, as well.”

Menner agrees with Schaefer that relationships are important. He claims, “We now are in a slightly more carrier- or capacity-friendly environment, with retailers constructing more productive relationships with carriers.” This has resulted from leading retailers embracing “a set of intelligent strategies” such as “sourcing strategies, developing longer-term contracts with transportation providers and taking other steps to be prepared for changing market dynamics.” He claims, “This is a change from the past few years, when the ball has been squarely in the shippers’ court, in terms of defining the commercial interaction with providers.” The article continues:

“At the same time, retailers are becoming more discerning and exacting around the service they expect from suppliers and logistics providers and more rigorous in the imposition of penalties for service lapses, Menner says. ‘Retailers have invested a lot in information systems that provide data on shipments all the way through the supply chain. They have a full understanding of how their partners are performing,’ he says. Instead of providing the basis for more confrontation, however, Menner says this knowledge seems, instead, to be supporting more constructive and improvement-oriented conversations. ‘We hear time and time again from our consumer packaged goods customers that the adversarial relationships they used to have with retailers were caused by a lack of understanding about where they were meeting customer expectations and where they were falling short. When the right information is gathered, and there is confidence in its accuracy, companies can use that data to analyze supply chain operations and present it internally and to partners as a basis for improvement,’ he says.”

Menner’s point that better collaboration reduces adversarial relationships is an important one. Supply chain stakeholders who are reluctant to collaborate should take note. Max Jeffrey notes that extended (i.e., international) supply chains present “some significant challenges with shipping or transportation – both in cost and also the transit time.” [“How do you handle the multiple dimensions of transportation management?” The 21st Century Supply Chain, 20 June 2011] He explains:

“The trade off is cost versus speed as to how to get the goods from Asia to North America: via air or sea. In an ideal world, and especially for bulky items, freight by sea is the most cost effective option and is used as the default shipment option. Shipments by sea can take around a month or even longer to reach the destination. Therefore, there are times when shipments need to be expedited to meet demand and air freight must be used. This is a classic supply chain problem: how to balance transportation costs against demand and supply. Once the decision to put the materials on a boat is committed to, these materials are basically unavailable for a month or more. This can be a real problem to have this in-transit inventory tied up when these materials are needed to fulfill shortages or customer demand.”

If customer demands change or shortages occur, you generally can’t re-route the ship to another port for offloading. A good optimization system, however, may be able to provide you with other alternatives. Jeffrey says that some software solutions remain too limited to solve all of the complexities involved. He explains:

“Some companies struggle with the issue of transportation, primarily because there are multiple considerations:

- “Which orders should be expedited to use air shipment?

- “Is the cost of the expedited shipment worth it?

- “How do you effectively communicate to suppliers which orders to expedite?

“Related to item 1, we need access to planning information to determine orders that potentially are late to demand. Adding in item 2, we need to be able to evaluate the cost of expediting against the additional revenue that can be realized in the current period with the expedited order. This implies that some sort of simulation capability needs to be present to model the change in the supply plan and how that will impact the fulfillment of demand. Item 3 has to do with the actual execution, purchase orders may need to be updated or at a minimum the change in shipping method needs to be clearly communicated to the supplier. The considerations or dimensions of the problem can be summarized as

- “plan/simulate,

- “calculate cost, and

- “execute.

“Many of the third party or extended modules available on the market today can only handle one or two of the three considerations. Therefore, the above considerations require a ‘one to many’ solution. The ideal solution is to have an application that enables all three of the dimensions: determining what needs to be expedited and the resulting impact on revenue and customer service; calculating the cost and benefit; and effective communication to suppliers and execution.”

This kind of “one to many” solution is exactly the kind of supply chain optimization in which Enterra Solutions specializes. We use a “sense, think/learn, and act” framework, where the sense portion of the system deals with the plan/simulate dimension pointed out by Jeffrey, the think/learn portion deals with the calculate cost dimension, and the act portion deals with execute dimension. Because these are large and complex challenges, we are dealing with them at a bite at a time, but the results have been encouraging.